Genesis and the origins of money

original article by Vijay Boyapati posted here

With the price of a bitcoin surging to new highs in 2017, the bullish case for investors might seem so obvious it does not need stating. Alternatively it may seem foolish to invest in a digital asset that isn’t backed by any commodity or government and whose price rise has prompted some to compare it to the tulip mania or the dot-com bubble. Neither is true; the bullish case for Bitcoin is compelling but far from obvious. There are significant risks to investing in Bitcoin, but, as I will argue, there is still an immense opportunity.

Genesis

Never in the history of the world had it been possible to transfer value between distant peoples without relying on a trusted intermediary, such as a bank or government. In 2008 Satoshi Nakamoto, whose identity is still unknown, published a 9 page solution to a long-standing problem of computer science known as the Byzantine General’s Problem. Nakamoto’s solution and the system he built from it — Bitcoin — allowed, for the first time ever, value to be quickly transferred, at great distance, in a completely trustless way. The ramifications of the creation of Bitcoin are so profound for both economics and computer science that Nakamoto should rightly be the first person to qualify for both a Nobel prize in Economics and the Turing award.

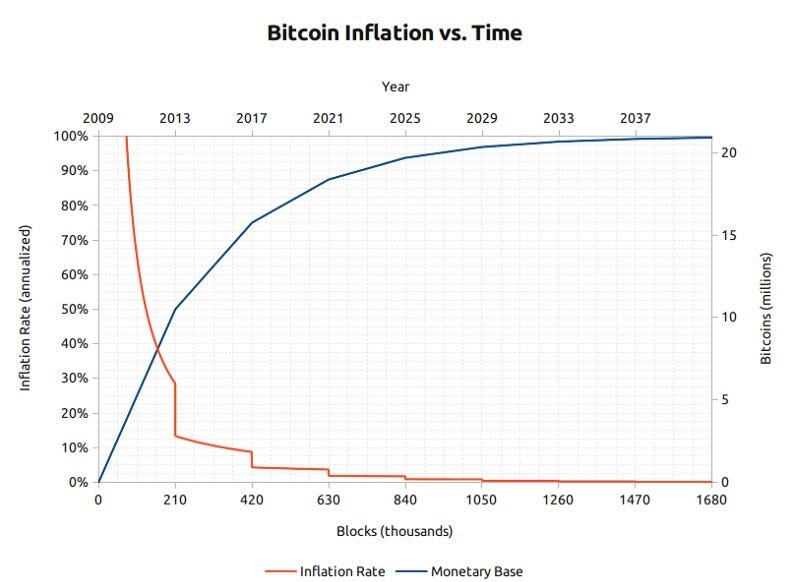

For an investor the salient fact of the invention of Bitcoin is the creation of a new scarce digital good — bitcoins. Bitcoins are transferable digital tokens that are created on the Bitcoin network in a process known as “mining”. Bitcoin mining is roughly analogous to gold mining except that production follows a designed, predictable schedule. By design, only 21 million bitcoins will ever be mined and most of these already have been — approximately 16.8 million bitcoins have been mined at the time of writing. Every four years the number of bitcoins produced by mining halves and the production of new bitcoins will end completely by the year 2140.

Bitcoins are not backed by any physical commodity, nor are they guaranteed by any government or company, which raises the obvious question for a new bitcoin investor: why do they have any value at all? Unlike stocks, bonds, real-estate or even commodities such as oil and wheat, bitcoins cannot be valued using standard discounted cash flow analysis or by demand for their use in the production of higher order goods. Bitcoins fall into an entirely different category of goods, known as monetary goods, whose value is set game theoretically. I.e., each market participant values the good based on their appraisal of whether and how much other participants will value it. To understand the game theoretic nature of monetary goods we need to explore the origins of money.

The Origins of Money

In the earliest human societies, trade between groups of people occurred through barter. The incredible inefficiencies inherent to barter trade drastically limited the scale and geographical scope at which trade could occur. A major disadvantage with barter based trade is the double coincidence of wants problem. An apple grower may desire trade with a fisherman, for example, but if the fisherman does not desire apples at the same moment, the trade will not take place. Over time humans evolved a desire to hold certain collectible items for their rarity and symbolic value (examples include shells, animal teeth and flint). Indeed, as Nick Szabo argues in his brilliant essay on the origins of money, the human desire for collectibles provided a distinct evolutionary advantage for early man over his nearest biological competitors, homo neanderthalis.

The primary and ultimate evolutionary function of collectibles was as a medium for storing and transferring wealth.

Collectibles served as a sort of “proto-money” by making trade possible between otherwise antagonistic tribes and by allowing wealth to be transferred between generations. Trade and transfer of collectibles were quite infrequent in paleolithic societies and these goods served more as a “store of value” rather than the “medium of exchange” role that we largely recognize modern money to play. Szabo explains:

Compared to modern money, primitive money had a very low velocity — it might be transferred only a handful of times in an average individual’s lifetime. Nevertheless, a durable collectible, what today we would call an heirloom, could persist for many generations and added substantial value at each transfer — often making the transfer even possible at all.

Early man faced an important game theoretic dilemma when deciding which collectibles to gather or create: which objects would be desired by other humans? By correctly anticipating which objects might be demanded for their collectible value, a tremendous benefit was conferred to the possessor in their ability to complete trade and to acquire wealth. Some Native American tribes such as the Narragansetts, specialized in the manufacture of otherwise useless collectibles simply for their value in trade. It is worth noting that the earlier the anticipation of future demand for a collectible good, the greater the advantage conferred to its possessor; it can be acquired more cheaply than when it is widely demanded and its trade value appreciates as the population which demands it expands. Furthermore, acquiring a good in hopes that it will be demanded as a future store of value hastens its adoption for that very purpose. This seeming circularity is actually a feedback loop that drives societies to quickly converge on a single store of value. In game theoretic terms this is known as a “Nash Equilibrium”. Achieving a Nash Equilibrium for a store of value is a major boon to any society as it greatly facilitates trade and the division of labor, paving the way for the advent of civilization.

Over the millennia, as human societies grew and trade routes developed, the stores of value that had emerged in individual societies came to compete against each other. Merchants and traders would face a choice of whether to save the proceeds of their trade in the store of value of their own society or the store of value of the society they were trading with, or some balance of both. The benefit of maintaining savings in a foreign store of value was the enhanced ability to complete trade in the associated foreign society. Merchants holding savings in a foreign store of value also had an incentive to encourage its adoption within their own society, as this would increase the purchasing power of their savings. The benefits of an imported store of value accrued not only to the merchants doing the importing, but also to the societies themselves. Two societies converging on a single store of value would see a substantial decrease in the cost of completing trade with each other and an attendant increase in trade based wealth. Indeed, the 19th century was the first time when most of the world converged on a single store of value — gold — and this period saw the greatest explosion of trade in the history of the world. Of this halcyon period, Lord Keynes wrote:

What an extraordinary episode in the economic progress of man that age was … for any man of capacity or character at all exceeding the average, into the middle and upper classes, for whom life offered, at a low cost and with the least trouble, conveniences, comforts, and amenities beyond the compass of the richest and most powerful monarchs of other ages. The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep

Continue to Part 2>>

In part 2, I will cover the attributes that make a good store of value and how Bitcoin compares to other monetary goods, such as gold and fiat currencies, across these attributes.

Follow us on facebook and get our notifications for more useful crypto info